Strategy 1: Delay Social Security

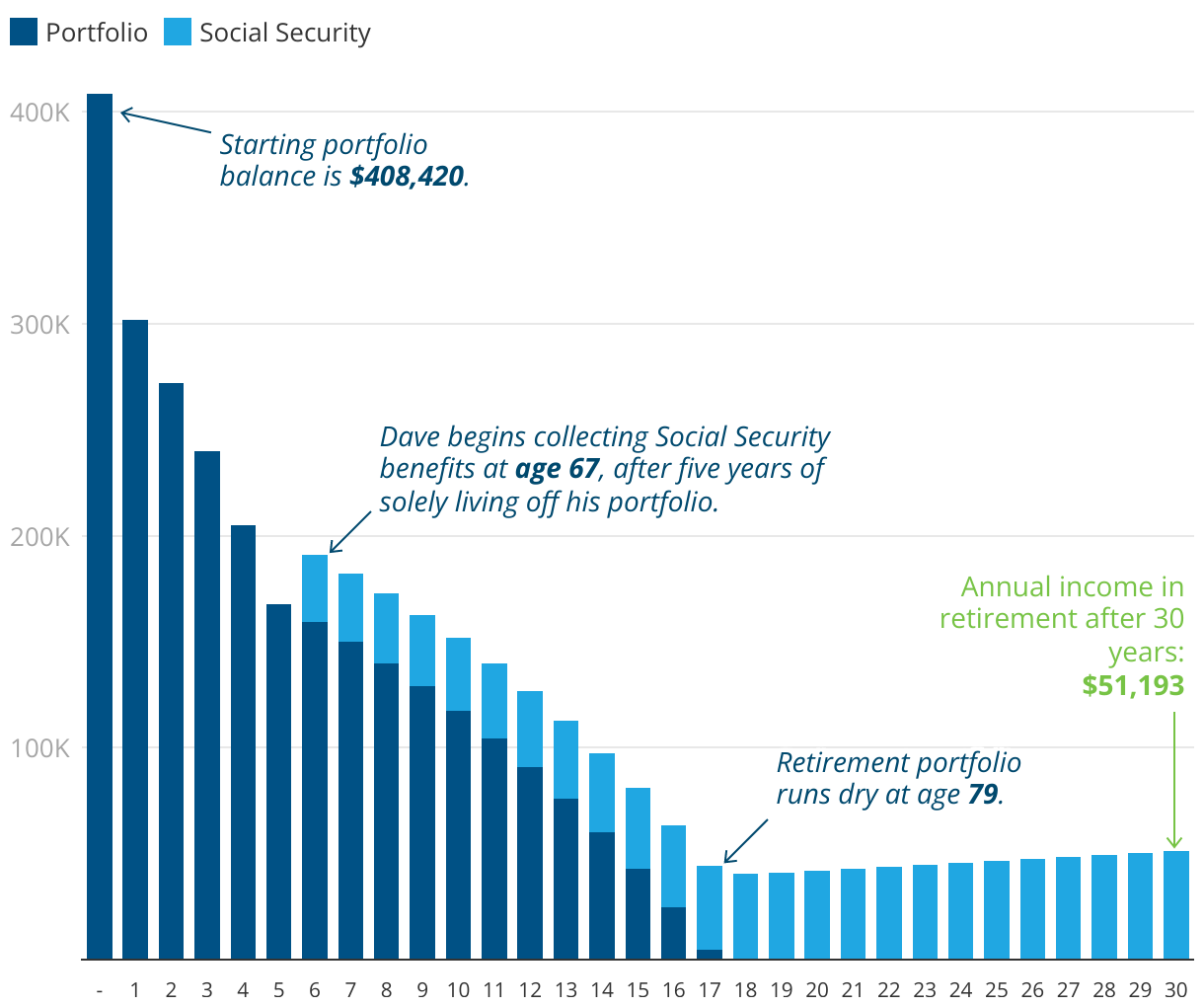

We considered a 30-year hypothetical scenario with an investor named Dave who has a 60/40 portfolio worth $408,420. This investor chooses to delay Social Security and live solely on portfolio withdrawals for the first five years of retirement. At age 67, he begins claiming Social Security benefits.

Image is a chart by SmartAsset titled "Strategy 1: Delay Social Security".