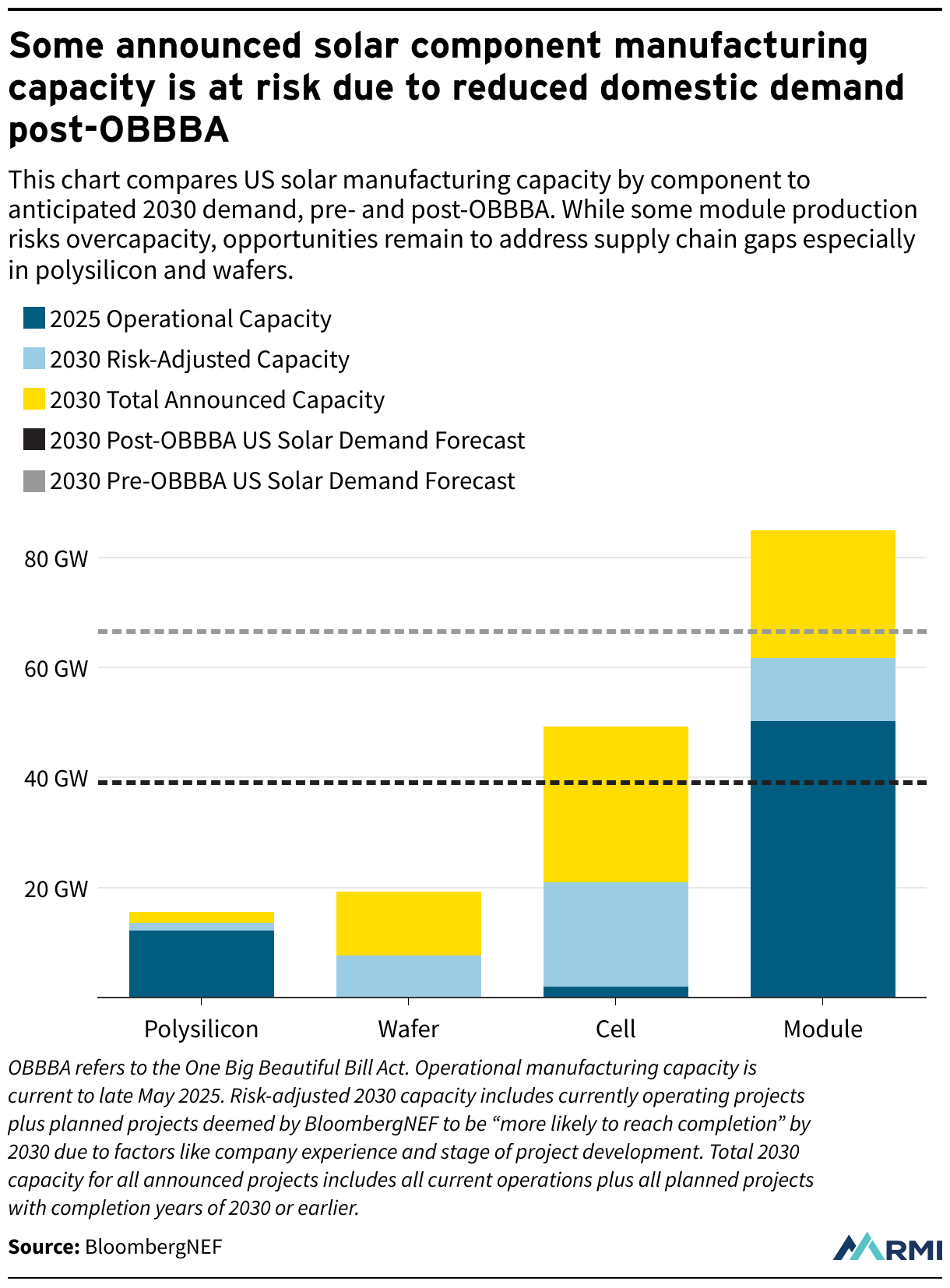

Some announced solar component manufacturing capacity is at risk due to reduced domestic demand post-OBBBA

This chart compares US solar manufacturing capacity by component to anticipated 2030 demand, pre- and post-OBBBA. While some module production risks overcapacity, opportunities remain to address supply chain gaps especially in polysilicon and wafers.

{kind=link}