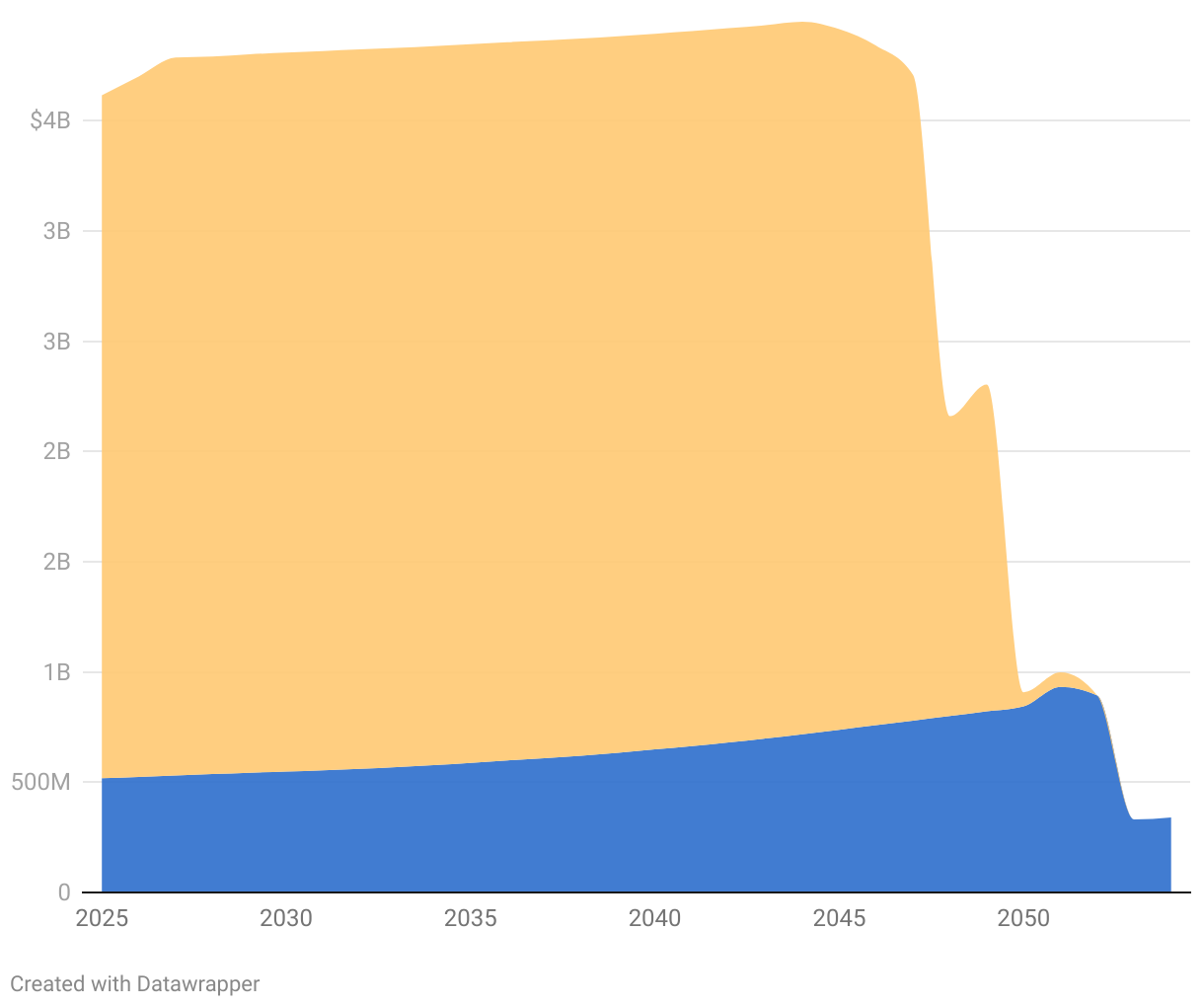

Connecticut will be paying off its pension debt for decades to come

Because of decades of improper funding, Connecticut's annual contribution to the pension fund has two components:

• A normal cost that involves setting aside funds for present-day employees' eventual retirement benefits.

• An unfunded liability component that covers the missed deposits of past generations and related lost investment opportunities.