Several Options to Modify the Child Tax Credit Would Have Modest Effects

on Parental Employment

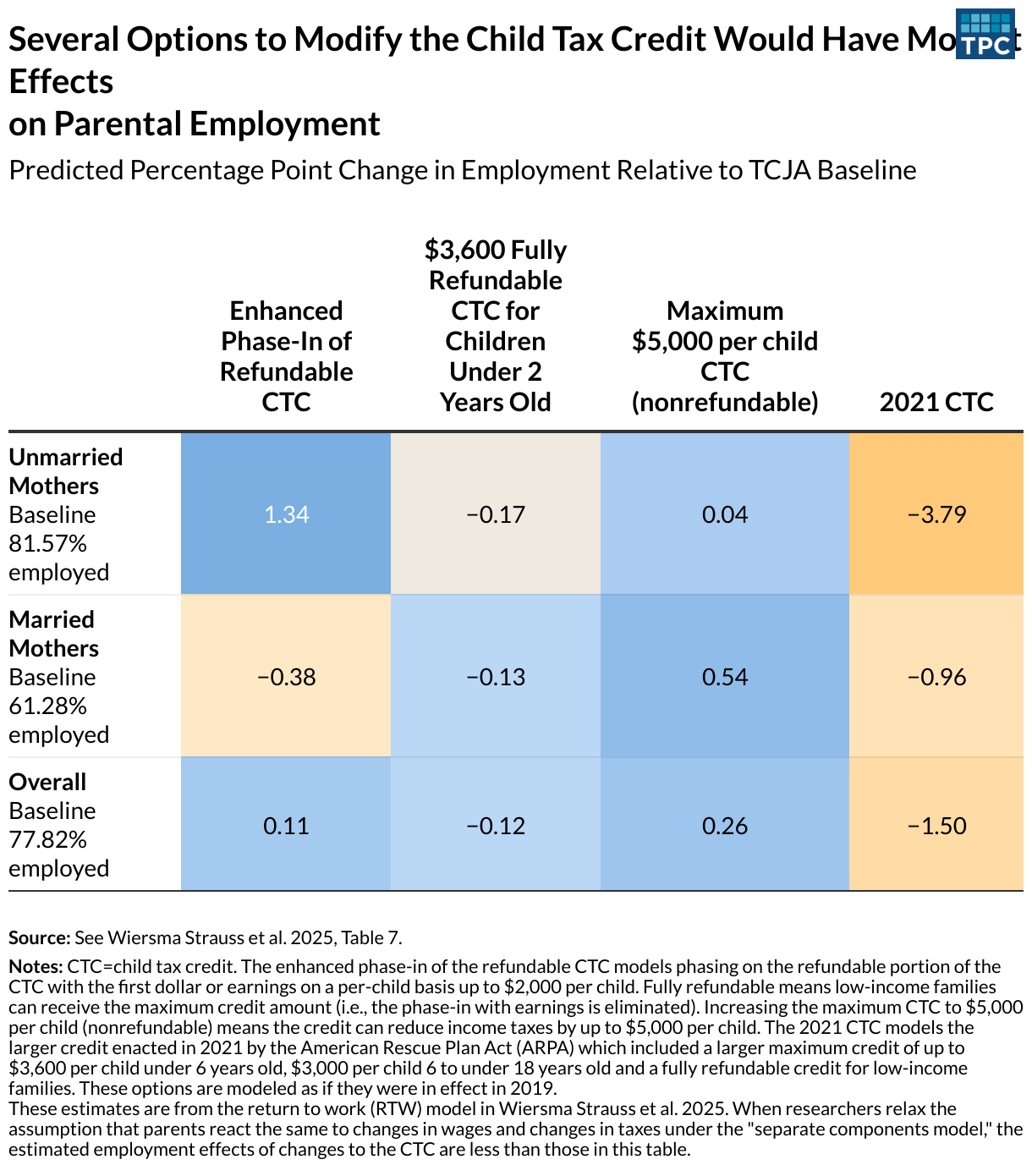

Predicted Percentage Point Change in Employment Relative to TCJA Baseline

Source: See

Wiersma Strauss et al. 2025, Table 7.

Notes: CTC=child tax credit. The enhanced phase-in of the refundable CTC models phasing on the refundable portion of the CTC with the first dollar or earnings on a per-child basis up to $2,000 per child. Fully refundable means low-income families can receive the maximum credit amount (i.e., the phase-in with earnings is eliminated). Increasing the maximum CTC to $5,000 per child (nonrefundable) means the credit can reduce income taxes by up to $5,000 per child. The 2021 CTC models the larger credit enacted in 2021 by the American Rescue Plan Act (ARPA) which included a larger maximum credit of up to $3,600 per child under 6 years old, $3,000 per child 6 to under 18 years old and a fully refundable credit for low-income families. These options are modeled as if they were in effect in 2019.

These estimates are from the return to work (RTW) model in Wiersma Strauss et al. 2025. When researchers relax the assumption that parents react the same to changes in wages and changes in taxes under the "separate components model," the estimated employment effects of changes to the CTC are less than those in this table.

These estimates are from the return to work (RTW) model in Wiersma Strauss et al. 2025. When researchers relax the assumption that parents react the same to changes in wages and changes in taxes under the "separate components model," the estimated employment effects of changes to the CTC are less than those in this table.

{kind=link}